Navigating Uncertainty - The Strategic Art of Tail Risk Hedging

Building resilience in long-term investment portfolios

Risk involves a choice rather than a fate or destiny

In his book "Against the Gods: The Remarkable Story of Risk," Peter Bernstein discusses the origin of the word "risk." He describes that the word "risk" derives from the early Italian word risicare, which means "to dare." This etymology highlights that risk involves a choice rather than a fate or destiny. The concept of risk, as Bernstein elaborates, is fundamentally about making decisions with uncertain outcomes, emphasizing the proactive nature of engaging with uncertainty. This understanding contrasts with views of risk that focus solely on the potential for loss or danger, framing risk instead as an essential part of decision-making and progress.

Indeed, in investing, we are paid for dealing with uncertainty and earning a risk premium. The business of investing is taking risks and making positive expected value bets.

This contrasts with other businesses where buying insurance against unrewarded risks makes economic sense. For example, a shipping company is rewarded for carrying goods from point A to point B, and losing their cargo to a hurricane is not a risk they get paid to take (not to mention the tragedy and potential loss of human life). Therefore, it's pretty clear that paying an insurance premium to compensate against financial loss may be in the best interest of the shipping company.

The case for hedging losses in investment portfolios is less clearcut, since the risk factor you are trying to hedge may be the same risk factor that is driving your return. If efficiently priced, the cost of hedging tail risk should negate the positive risk premium earned from the investments being made.

In theory, long-term investors may be statistically better off riding out drawdowns than implementing systematic hedging programs.

So Why Hedge a Rewarded Risk?

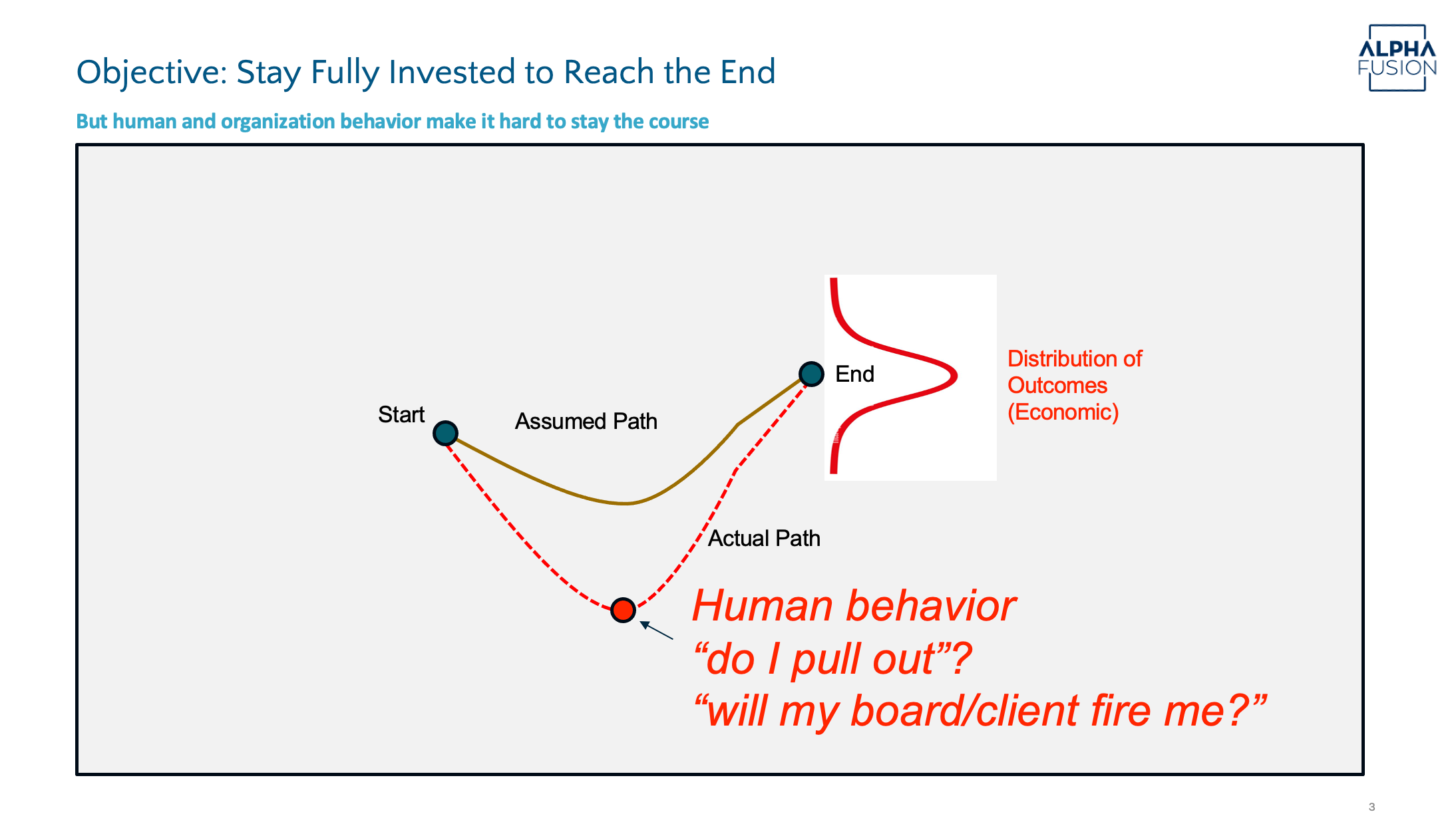

Because theory may not be given enough time to work in the real world. It is hard for most investors to stay fully invested and not change their strategy in the face of significant drawdowns. Our emotions, the governance structures of our clients, and potential for margin calls in levered portfolios make staying fully invested through drawdowns challenging.

For portfolios to meet strategic long-run expectations, an investor needs to remain fully and continuously invested, and not sell prematurely and crystallize permanent losses. Therefore, the utility of an investor increases by adopting any strategy that prevents them from ‘breaking the compounding machine’ - e.g., by avoiding being forced to reduce positions prematurely, or by lowering odds of suffering a permanent loss of capital. Chart 1 illustrates this concept.

In this article I discuss how to approach Tail Risk Hedging as a strategic (as opposed to tactical) component for portfolios that seek staying power through an extreme drawdown scenario, assuming that the timing of that drawdown event is unpredictable.

Why Manage Drawdown Risk?

Recovery from a sharp drawdown reduces power of compounding – e.g. you need 11% to recover from a 10% drawdown but you need 100% to recover from a 50% drawdown. In levered portfolios, drawdowns require posting collateral and can impact level of risk we take

How to Design a Tail Hedging Program?

The optimal tail hedging strategy is one that minimizes costs during normal markets (e.g. 95% of scenarios) while offering desired payoff in the 5% of ‘bad’ scenarios.

Questions that help frame a tail hedge program:

When does it need to work? A tail hedging program ought to focus on extreme events, and be comfortable with the hedge not being reactive under ‘normal’ scenarios. For example, in an equity portfolio you might want to have staying power in a GFC type scenario.

What drawdown shape are you looking to protect? Drawdowns can be prolonged or sharp. Prolonged typically occur when there is a shift in an economic regime, over a period of several months, perhaps even years. Tail risk programs aren’t designed for prolonged drawdowns, and asset allocation may be a better tool for regime based drawdowns. On the other hand, sharp drawdowns that are the result of a major shock, are the types of drawdowns tail risk hedging is meant to protect - these events are ones where the probability of recovery is high, assuming you can survive the shock.

How much? Do you need to hedge 100% or only enough to remain invested through that extreme event (e.g. would 70% payoff work?)

Precision? If the extreme risk in your portfolio is driven mainly by equity beta, then perhaps using a liquid index may be less expensive while having a similar desired payoff in extreme markets.

Hedging Instruments

The goal of a hedging program is to maximize payoff in the ‘extreme’ environment while minimizing negative carry under ‘normal’ environments. Since this violates the ‘no free lunch’ principle, we need to be willing to make trade-offs.

I find combining “contractual” payoffs that have a high certainty of being effective (such as out of the money put options) with “coincidental” strategies that are uncorrelated / diversify equity risk to be a useful framework, as illustrated in the chart below. The trade-off that I am willing to make here is that these “coincidental” strategies have a high probability but are not certain to pay off. However, I may be willing to take the uncertainty in exchange for the reduction in negative carry.

Integrate Hedging with the Underlying

The most important aspect of a hedging program is that the hedge needs to be an integral part of the portfolio, and combined with a funding source. Otherwise you suffer from the 99% loss and liquidation scenarios that some independent tail risk hedging strategies have faced. For that reason I prefer combining capital efficient tail hedges with an underlying portfolio/beta instead of maintaining a standalone hedging program.

Results

If designed appropriately, a tail hedging program can suffer low/moderate negative carry during most ‘normal’ scenarios, while offering a positive asymmetric return in the extreme scenarios that you seek protection.

The charts below show the output of a hypothetical hedging strategy from a research model (Not Investment Advice). Using a combination of strategies may be superior to a program that relies solely on purchasing puts. I find it interesting (and obvious in hindsight) that a hedging program is likely to be positive only if the events that are being hedged occur.

Reach out directly to me if you would like to discuss specifics.

In a future post, we will get into the other side of the risk equation - i.e. when might it be appropriate to take tail risk.